Foreign Trustee Of Us Trust

Logo And Website Design For Antipodes Trust Group Ltd Business Blog Design Website Design Entrepreneur Website

Trusteins Estate Planning Trust How To Plan

Https Www Gerberco Com Wealth Transfer Pdf

Common Law Trust Setup Common Law Trust Law

International Asset Protection Trust Assetprotection Com

How Does Capitus Diminutio Minimia Affect Us In Fake Fraud Courts With Images Fraud We Energies Court

How is a foreign trust taxed by the us.

Foreign trustee of us trust. Person who is treated as the owner of a foreign trust under the grantor trust rules irc sections 671 679 is taxed on the income of that trust. But before a trustee can be chosen it is crucial to understand the difference between a domestic trust and a foreign trust. Citizen who resides in another country as a successor trustee the trust could be considered a foreign trust by the irs resulting in adverse tax consequences. Most foreign trusts created by u s.

A foreign trust is also considered a grantor trust for u s. Irc section 679 applies specifically in the context of foreign trusts and will treat as an owner of a foreign trust a u s. When the grantor retains an incidence of ownership over the assets transferred to a trust it is treated as a grantor trust under irc sec. Beneficiaries of any portion of the trust.

Citizen or a u s. Grantors have at least one current or future u s. Grantor makes a gratuitous transfer to a foreign trust which has one or more u s. These trusts are called foreign grantor trusts fgts and at the time that the grantor dies then it is usually beneficial to domesticate the trust and that is simply accomplished with us hybrid trusts by having the foreign controlling person retire and that automatically converts the trust into a us domestic trust.

However if a trust names a non u s. Most foreign trustees however are unfamiliar with these concepts and potential tax traps for us beneficiaries. The withholding requirement applies to any person making a payment. And foreign beneficiaries on accumulation distributions from a foreign trust however is different.

To put it simply a trust is a foreign trust if it is not treated as a domestic trust. If your living trust or other trusts created after your death are treated as foreign trusts then payments made to those trusts are generally subject to a 30 income tax withholding requirement unless modified by a tax treaty with the country of the foreign trustee. Person who transfers assets. Income tax purposes when a u s.

Tax purposes trusts are taxed as grantor or non grantor trusts. Beneficiaries of a nongrantor foreign trust are generally taxable on the currently distributed income of the trust in the same manner as the beneficiaries of domestic trusts. For us trust and estate advisors it is standard practice to manage the tax issues surrounding the use of passive foreign investment companies and the need to regulate the attribution and payment of annual distributable net income. Beneficiaries or potential u s.

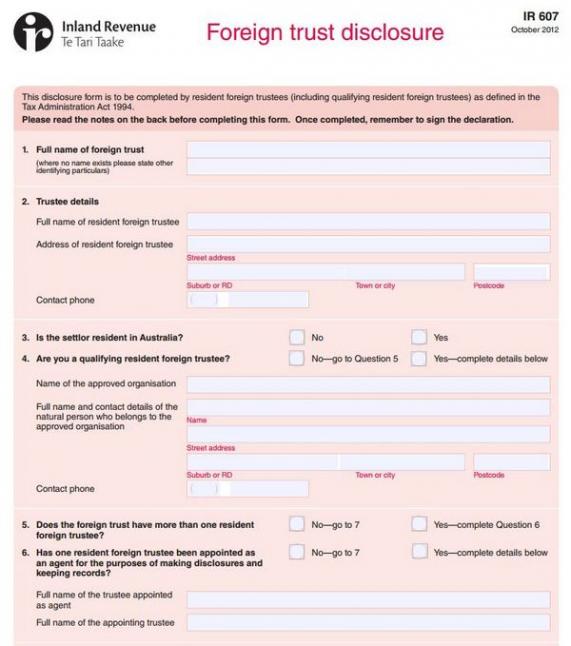

The selection of a successor trustee for a living trust requires practical thinking. Trustee files fbar to report foreign accounts by 15 april a trust subject to the laws of a us state and administered by a us trust company can still be classified as foreign if it fails the.

Taxation Of Trust Net Income Non Resident Beneficiaries Australian Taxation Office

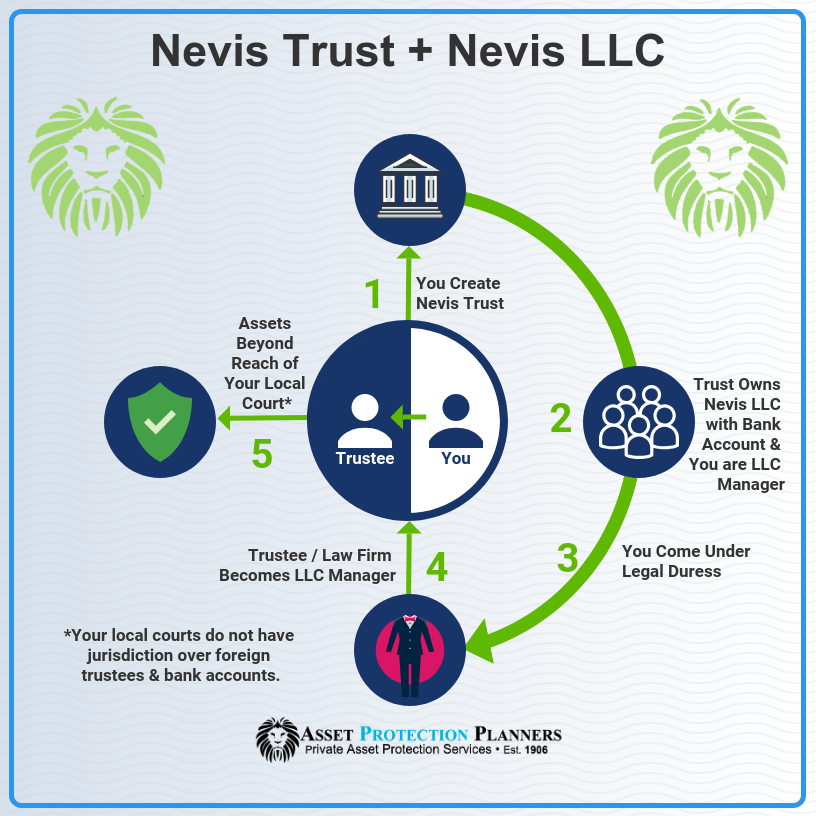

Nevis Trust And Company Formation For Offshore Asset Protection

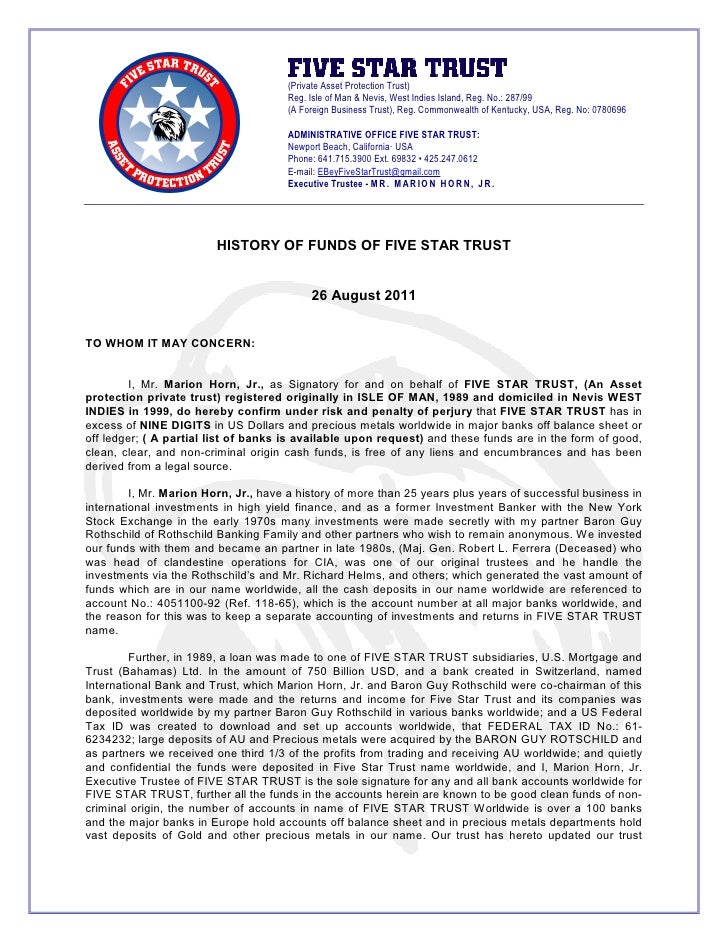

History Of Five Star Trust Funds

Offshore Asset Protection Trust Formation And Accounts Alper Law

3 22 19 Foreign Trust System Internal Revenue Service

Oooqnfdrtipozm

Aerospace Trust Management Llc Provides Aircraft Owner Trustee Services For Us And Non Us Citize Federal Aviation Administration Aerospace Aircraft Maintenance

Arka Provides You Valuable Information Through Its News And Insight Section Read Informative News And Keep Yours Cayman Islands Estate Planning Legal Services

Pin On Survival

Public Ruling Lta000 3 1 Foreign Corporations And Foreign Trusts Interests Of Foreign Persons And Related Persons Queensland Treasury

Sample Letter To Send To The Accountant Re Oscar

Variation Of Discretionary Trust Exclude Foreign Persons Free Template Sample Lawpath

Http Publications Ruchelaw Com News 2016 08 Tax101 Us Trust Foreign Settlor Pdf